Thinking About Selling Your Healthcare Practice? Read This First.

At Beaird Harris, we understand that selling a medical or dental practice isn’t just a financial decision—it’s a deeply personal one. After years of serving…

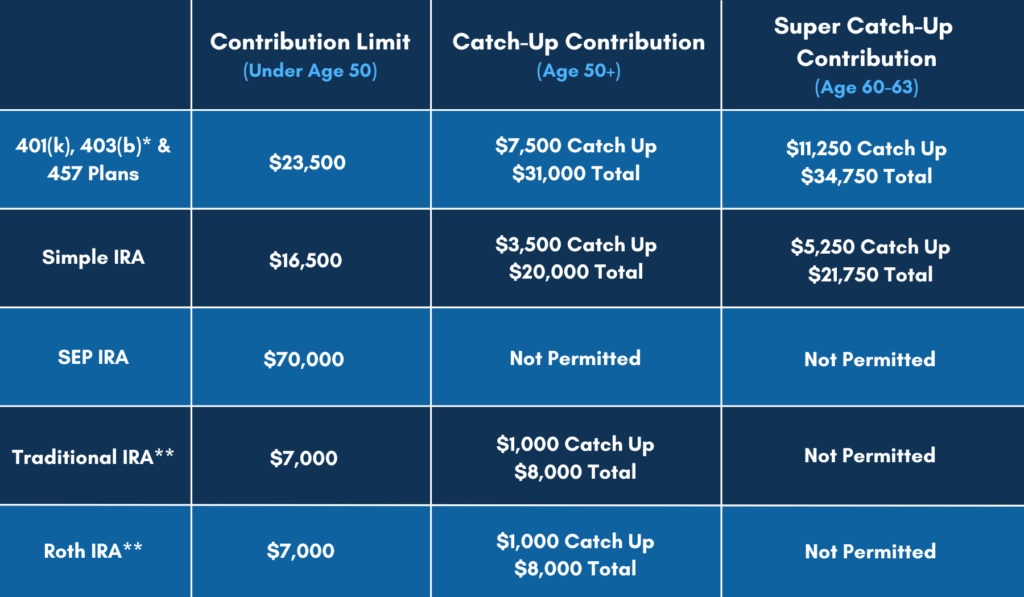

In 2025, most employees can put up to $23,500 into their 401k and similar retirement plans. People 50 years or older (as of December 31st, 2025) can add an extra $7,500 to help grow their savings as they get closer to retirement age. This is called a catch-up contribution, which increases their total possible contribution to $31,000.

In 2025, people 60-63 years old (as of December 31, 2025) will get a special savings opportunity called a “super” catch-up contribution, where employees can add an extra $11,250 to their usual maximum 401k contributions, increasing their total possible contribution to $34,750. However, once you turn 64, your contribution limit will revert back to the 50+ catch-up limit of $7,500.

*Employees with at least 15 years of service may be eligible to make additional contributions to a 403(b) plan in addition to the regular catch-up for participants who are age 50 or over. **Subject to income limitations.

*Employees with at least 15 years of service may be eligible to make additional contributions to a 403(b) plan in addition to the regular catch-up for participants who are age 50 or over. **Subject to income limitations.The good news? You don’t have to wait for your actual birthday to get started. You’re eligible to start contributing extra the year you hit 50 for catch-up contributions or 60-63 for super catch-up contributions!

How to Get Started

To begin making these additional contributions, you will need to:

Important Deadlines to Remember:

Why This Matters

The ability to increase your retirement contributions during the final stretch of your career can make a significant difference in your financial security. These changes offer a valuable opportunity to accelerate savings and ensure you’re on track to meet your retirement goals.

If you have questions about how these changes fit into your retirement strategy or need assistance adjusting your contributions, feel free to reach out. We’re here to help you take full advantage of these new provisions and keep your retirement planning on track.

At Beaird Harris, we understand that selling a medical or dental practice isn’t just a financial decision—it’s a deeply personal one. After years of serving…

Now that another tax season is in the rearview mirror, what lessons can you take from this year’s filing experience to strengthen your financial future?

Proper classification of meal expenses can help businesses maximize deductions while staying compliant with IRS regulations. Here’s what business owners need to know: 1. 50%…